What Is Tax Diversification?

Tax diversification means spreading your investments across accounts with different tax treatments—rather than putting all your money into one type of account. Just like investment diversification helps manage risk, tax diversification prepares you to face different tax scenarios and makes your withdrawals more flexible in the future.

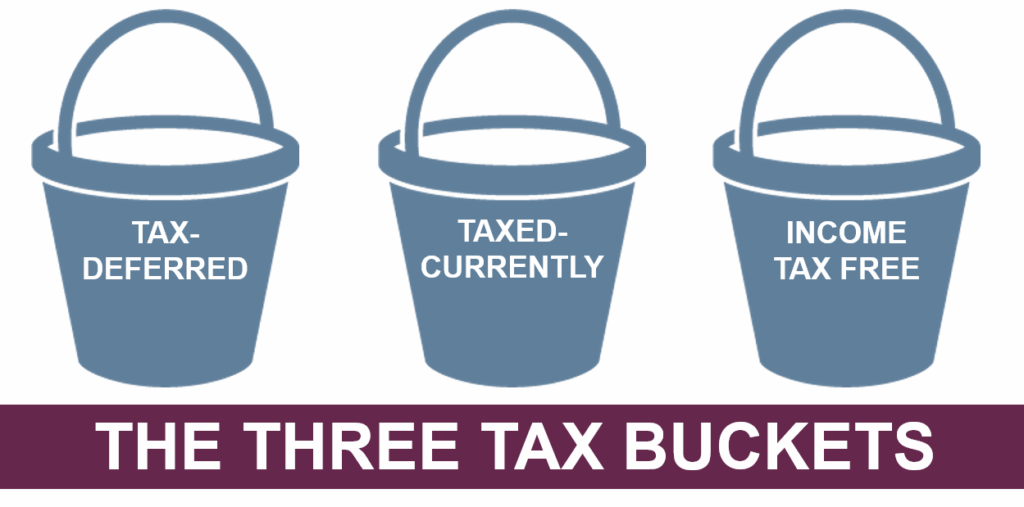

The Three Main Tax Buckets

There are three primary types of tax treatment for investment accounts:

- Tax-Deferred Accounts

- Examples: Traditional IRAs, 401(k)s

- How it works: Contributions may be tax-deductible and investments grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Tax-Free Accounts

- Examples: Roth IRAs, Roth 401(k)s

- How it works: You pay taxes on contributions now, but investments grow tax-free and qualified withdrawals in retirement aren’t taxed.

- Taxable Accounts

- Examples: Brokerage accounts, bank savings

- How it works: Investments are funded with after-tax dollars, and you pay taxes on dividends, interest, and capital gains annually—but you get flexibility and control over withdrawals.

Why Tax Diversification Matters

1. Flexibility in Retirement:

When you retire, having money spread among the three buckets means you can choose which account to withdraw from depending on your income needs and the tax climate that year.

2. Tax-Efficient Withdrawals:

If tax rates rise, drawing from tax-free accounts like Roth IRAs could help you keep more money. If they drop, tax-deferred withdrawals may make sense.

3. Managing Required Minimum Distributions (RMDs):

Tax-deferred accounts come with required minimum distributions starting at a certain age. Tax-free accounts, like Roth IRAs, do not—giving you more freedom after retirement.

4. Estate Planning Benefits:

Some accounts are more favorable for leaving money to heirs. Roth accounts, for example, provide tax-free assets to beneficiaries.

Tax Diversification for Pre-Retirees

If you’re in your 50s or early 60s, pre-retirement is an ideal time to assess your tax diversification strategy and make any adjustments:

- Maximize Contributions: Consider contributing to both traditional and Roth retirement accounts if eligible. If your employer offers a Roth 401(k), take advantage of it.

- Use Catch-Up Contributions: Individuals over 50 can contribute extra to IRAs and 401(k)s, which can help boost balances across different tax buckets.

- Strategically Convert Traditional IRA Assets: Roth IRA conversions can be done gradually to spread out the tax impact.

- Build Taxable Savings: Regular investments in a brokerage account add another layer of flexibility—you won’t face penalties for withdrawals before age 59½.

- Review Projected RMDs: Estimate your required minimum distributions, so you’re not hit with unexpectedly large taxable income in retirement.

- Consider Future Tax Rates: Retirement might mean lower income/tax rates—but not always! Factor in possible changes to your income, deductions, and government policy.

Tax Diversification for Retirees

If you’ve entered retirement, you still have opportunities to take advantage of tax diversification:

- Coordinate Withdrawals: Use a combination of taxable, tax-deferred, and tax-free accounts. For example, withdraw enough from taxable accounts to fill lower tax brackets, then supplement with tax-free withdrawals.

- Manage RMDs: Satisfy your required minimum distributions from tax-deferred accounts, but consider if you can direct other needs from Roth or taxable buckets.

- Control Taxable Income: Withdrawals from Roth accounts don’t add to taxable income, which can help keep Social Security benefits tax-free or reduce Medicare premium surcharges.

- Leverage Charitable Giving: If you’re charitably inclined, direct RMDs to charities for a qualified charitable distribution, reducing taxable income.

- Review Estate Benefits: Roth accounts can be left to heirs tax-free, and taxable accounts get a step-up in basis at death, which can minimize taxes for beneficiaries.

Final Thoughts

Whether you’re approaching retirement or already enjoying it, tax diversification is a powerful strategy for controlling your retirement income, minimizing surprise tax bills, and passing on more to loved ones.

Mixing tax-deferred, tax-free, and taxable accounts allows you to adapt to new tax laws, optimize withdrawals for each phase of retirement, and keep more control over your financial future.

Want to discover how tax diversification fits into your retirement plan? Schedule a personalized review today—let’s build a strategy together that works for you!