When the Federal Reserve announces an interest rate cut, it often makes headlines and sparks conversations across the financial world. But what does it really mean for investors, especially those nearing or in retirement? While each cycle is different, history gives us some perspective on how the stock market has behaved in the months following these policy moves.

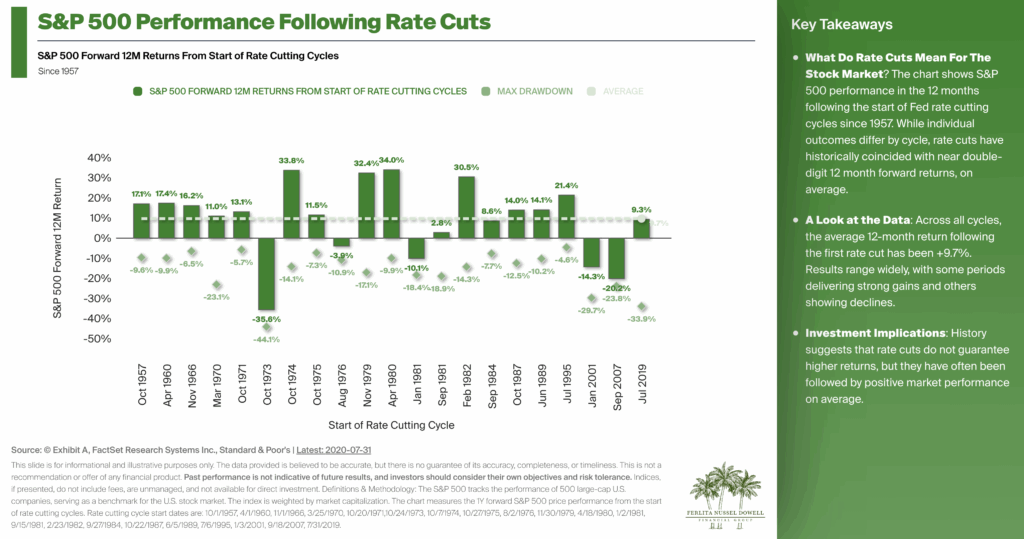

The chart above tracks S&P 500 forward 12-month returns from the start of every Fed rate cutting cycle since 1957. The data shows that, on average, markets have delivered +9.7% returns in the year after rate cuts begin. That’s a compelling figure, but it’s important to dig deeper into the details.

What the Data Tells Us

- Encouraging Averages: Across all cycles, the average return of nearly 10% is notable. In many instances, rate cuts provided support to the market and fueled strong rebounds. For example, in the early 1980s and mid-1970s, markets saw 30%+ gains in the year following cuts.

- Wide Range of Outcomes: Not every period produced gains. There were times, such as the early 1970s and the Great Financial Crisis in 2007–2008, when returns were negative despite Fed easing. This highlights that rate cuts do not guarantee positive results.

- Market Volatility Still Matters: Alongside returns, the chart also shows the maximum drawdowns—the largest temporary losses within those 12-month windows. Even in years that finished strong, investors still had to endure periods of double-digit declines.

Why Rate Cuts Impact the Market

The Fed typically lowers interest rates to stimulate the economy—reducing borrowing costs for businesses and consumers, encouraging spending and investment, and supporting growth. For the stock market, lower rates can mean:

- Cheaper borrowing costs for companies, which may boost profits and expansion.

- Attractive alternatives compared to bonds and savings accounts, which can push more money into equities.

- Improved investor sentiment, as markets often view cuts as a sign that the Fed is taking action to support growth.

However, it’s also worth noting that rate cuts usually occur in response to economic slowdowns or uncertainty. That means the backdrop isn’t always positive—and explains why results vary from cycle to cycle.

What It Means for Retirees and Pre-Retirees

For investors approaching or living in retirement, rate cuts can have mixed effects:

- Equity Portfolios: Potential for growth, but with risk of volatility. A strong year can boost retirement account balances, while downturns can test withdrawal strategies.

- Fixed Income Investments: Lower rates often mean lower yields on bonds and CDs, which can reduce income for conservative investors.

- Planning Implications: Retirees need to balance growth opportunities with protection. A guardrail strategy—where income withdrawals adjust depending on market performance—can help provide stability through uncertain times.

Final Thoughts

History shows that rate cuts have often been followed by positive market performance, but they are not a guarantee of success. The wide range of outcomes reminds us that timing the market or relying on averages can be risky. Instead, the most effective strategy is a personalized financial plan that prepares you for both the opportunities and the challenges that come with economic shifts.